This is a follow up blog to the Climate Tech Crux Move, published in January by Stafford Lloyd and Lea Simpson. Where we explored our shared theory that we already have the technical knowhow and financial resources to solve the climate crisis and reach net zero emissions. Exploring why, despite having all of that, so little was happening to get us to net zero.

Solutions and barriers

We believe the solutions are out there but there are systemic barriers preventing things from scaling. Often these barriers are invisible, intangible and more complex to grasp when compared to ‘just’ developing tech, which is way more tangible and simpler to determine cause and effect. The crux move is a useful analogy to begin to identify, unpack and tackle unseen barriers.

To explore this hypothesis further, we asked readers ‘what are the climate tech crux moves needed to break the climate change stalemate we find ourselves in?’. And we promised to revisit the blog and publish findings. So here they are!

Survey contributors

Thank you to those who contributed, we received a total of 58 ideas from 22 people. Half came from climate tech innovators. Followed by advisors and then consultants as the second largest groups. Many of the responses came from those working on net zero in one form or another.

How we analysed survey responses

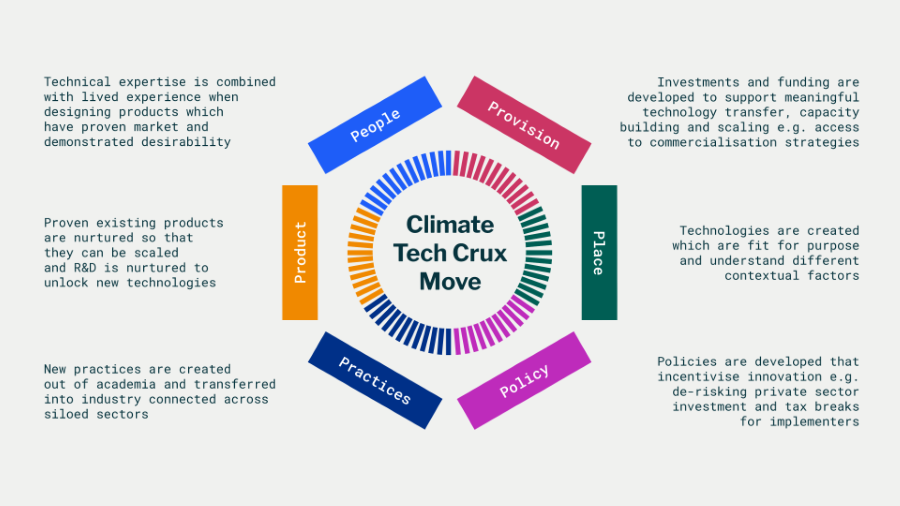

We analysed these responses using our 6P framework for systems thinking, which situates these tech products within a range of other systemic factors as outlined in the following diagram.

Diagram: the Climate Tech Crux Move six Ps

Description of Climate Tech Crux Move six Ps diagram

The Climate Tech Crux Move six Ps are:

- people: technical expertise is combined with lived experience when designing products which have proved market and demonstrated desirability

- provision: investment and funding are developed to support meaningful technology transfer, capacity building and scaling for example access to commercialisation strategies

- place: technologies are created which are fit for purpose and understand different contextual factors

- policy: policies are developed that incentivise innovation for example de-risking private sector investment and tax breaks for implementers

- practices: new practices are created out of academia and transferred into industry connected across siloed sectors

- product: proven existing products are nurtured so that they can be scales and research and development (R&D) is nurtured to unlock new technologies

Analysis

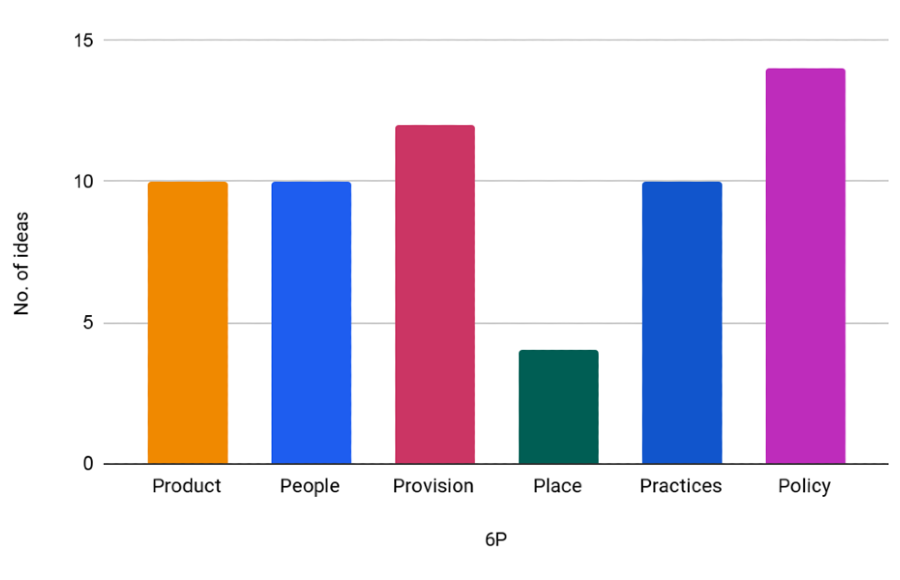

The analysis has been broken down by the P the solution was most aligned to. A snapshot of the results is in the following graph, but don’t be fooled by the graph; many of the ideas were linked or dependent on another P.

Bar chart: number of ideas contributed on the survey shown in relation to each of the six Ps

Description of survey results bar chart

Bar chart depicting how many ideas were received across the six Ps. We received:

- 10 ideas for product

- 10 ideas for people

- 12 ideas for provision

- four for place

- 10 for practices

- 14 for policy

What you told us

This is what you told us…

The most notable crux move is deceptively simple: collaboration and coordination. There is a strong need to increase collaboration and coordination across disciplines and sectors in the entire climate tech value chain to achieve effective policies, investment, uptake, and innovation. Never before has there been a greater need to upgrade the old maxim ‘innovate or die’ with a new one: ‘collaborate or die!’

Taking a closer look at the themes that emerged across the Ps (please note that the quotes have been included verbatim, so please excuse any typos or grammar mistakes!):

Product

Unsurprisingly, there were many innovative tech solutions resulting from R&D investment. These included synthetic hydrocarbons for renewable energy storage and solutions focusing on carbon dioxide concentration in the oceans, such as giant kelp. Scaling out known solutions that promise incremental energy efficiency gains, like double glazed windows, and products that support existing renewable energy technologies were also highlighted.

The question we ask is: what factors will enable these solutions to accelerate progress and scale? Which purchasing and market behaviours need to be shifted?

The current economic case for investment leads to capacity which… (~12-hour energy) storage capacity. If renewable generation is increased, longer-term energy storage capacity needs to be introduced to the grid (e.g., stores energy for 1 week+). However, this is not the best economical solution for sizing storage capacity… allowing accurate pricing in the energy market. For example, when it is cold and not windy for a week, increased peak energy prices could make longer-term storage more economically viable.

Policy

While there were many ‘standard’ solutions, such as introducing and updating regulations, some policy solutions pointed towards a more systemic approach to policy design. For instance, creating policies that embed both commercial and cultural incentives to facilitate the transition. Removing policy silos. Encouraging greater collaboration across departments and sectors. As well as making policies open and accessible.

Removal of policy silos around waste, carbon, and biodiversity. Common goals and language and incentives for collaboration, and as a result greater, faster impacts across all areas.

Practices

The main theme revolved around creating new practices to disrupt the status quo. This included collaborating and coordinating with key stakeholders and engaging incumbent legacy blockers in the conversation. Co-designing policies with innovators from the start was also highlighted.

Many organisations and innovators working in isolation… [on variations of the same tech].

A war effort approach to reducing red tape around bringing low carbon innovations to market. Cutting through and accelerating innovation by insisting on collaboration (including landscape & peer review and sharing of data/learning) in return for incentives to enable faster commercialisation.

Provision

A wide range of provision crux solutions were identified. These ranged from capacity building on climate and tech literacy across sectors in the climate tech value chain (investors, innovators, users). To designing niche and innovative investment vehicles, such as funds that test solutions covering multiple parts of the system, and new financing mechanisms like bonds to incentivise bulk purchase agreements.

Technology is aligned to solve several known business problems simultaneously, with Net zero being the main beneficiary. Stand-alone carbon solutions rely on goodwill and have slower adoption.

People

Most responses focused on shifting people’s behaviours and attitudes towards climate tech across the entire system, from end-users to workers in the climate tech value chain. Various methods were suggested, including communication campaigns, aligning purchasing incentives, and supply chain engagement programmes through peer learning or exchange partnerships.

Offer value such as cost savings on energy bills, carbon emissions reduction, asset value improvements, along with access to green financing seamlessly.

Place

A clear theme emerged around connecting communities to solutions, making them more motivated to engage in their success either financially or by better understanding the solution. This could be achieved through community ownership models or co-implementation of solutions with communities.

Take communities with you on the journey because they’ll be the implementers, the disciples, and the beneficiaries.

The crux of the crux!

So what’s the crux of net zero? The answer lies in being able to “identify the blockers and blast them away,” as beautifully put by one of our colleagues! The responses and findings have been valuable in testing our theory.

Broadly speaking, the findings of this small (yet well-formed) survey support the early conclusions outlined in our original blog.

First, fragmentation is a blocker that could be overcome through a more mission-oriented approach designed for cross-sector collaboration and pooled resources. The second blocker is human behaviour. Here, we’re not referring to consumer behaviours at the end of the value chain, but rather the behaviours of those we seek to galvanise. Collaborating across sectors is easier said than done. Establishing working relationships that promote trust, psychological safety, and mutual benefits is a daunting challenge.

One tangible example that we feel embodies more of this approach is the company cohort that forms part of Innovate UK’s Net Zero Heat programme. It has a clear mission to get the UK off gas for domestic heating. Convenes a variety of companies and stakeholders across the value chain, ecosystem and adjacent sectors to identify the main challenges. And uses this collective will for change to drive action. For example, on the need to upgrade building energy performance certificates, which is a key barrier for the scale out of new technologies in this sector.

At Innovate UK and Brink, we strongly believe in the power of convening. It’s a significant part of what we do. We recognise the need to deeply engage in specific sectors or solutions. Rally the entire value chain and system together and identify and test the crucial factors that can make a meaningful difference. We welcome any reflections on the survey findings.

Further information

Connect with Stafford on LinkedIn

Connect with Brink on LinkedIn

Connect with Innovate UK on LinkedIn

Follow Innovate UK on Facebook

Go to the new Innovate UK website

Go to the Innovate UK EDGE website

Sign up for our newsletter for the latest updates

Dr Stafford Lloyd recently helped develop Innovate UK’s net zero strategy and is now working on a new programme looking at how we can get more investment flowing into climate tech.

Stafford has a varied background in research, innovation, engineering and clean tech, working within small and large businesses. Feel free to connect with Stafford on LinkedIn.

Lea is Co-founder of Brink and the director of a number of innovation funds designed to make a positive impact across global education, health, and climate.

She has over 20 years’ experience working from California to Kathmandu on all thing’s tech, innovation and supporting organisations and governments to get fit for the future.

Lea has worked with partners to launch and run:

- Frontier Technologies Hub

- EdTech Hub

- Assistive Tech Innovation Fund

- Vaccine CoLab, Oxygen CoLab and more

Lea has pioneered approaches to solving systemic problems through CoLabs, where diverse groups are brought together to imagine radically better scenarios collectively (co) and then test them in the real world (lab).

To date the CoLabs have come together around vaccine data and uptake, oxygen provision for low-resource settings, cancer-related fatigue, and circular economy across informal sectors.